Daniel Sutherland, Data Analyst

19/12/2024 | EnergyPulse

Battery storage capacity in the UK: the state of the pipeline

19 December 2024 - EnergyPulse blog

Welcome to the inaugural EnergyPulse blog. I am Daniel Sutherland, a Data Analyst in the EnergyPulse team with a focus on the UK onshore wind and battery storage capacity pipelines.

In this blog series, we will dive into the project data tracked by EnergyPulse and how you can use it to understand project development of renewable energy.

This post investigates the state of the UK battery storage pipeline, year-to-date figures and an insight into the appetite to develop over time.

Battery storage is essential for providing the security and flexibility that will make our future energy system resilient and reliable. Effective use of battery storage will also provide energy system cost savings and benefits for businesses and consumers by enabling energy that is produced at times of high generation be stored and used during peak demand times.

Currently there are 2469 energy storage projects tracked in the EnergyPulse database (including inactive projects, as of 18/11/2024), covering details such as project capacity, development status, developer and ownership, location and more.

Daniel Sutherland, EnergyPulse Data Analyst

The UK battery storage pipeline at a glance

1659 active UK battery storage projects

5,013MW total operational capacity

127,404MW in the pipeline

960.9MW capacity commissioned in 2024 to date

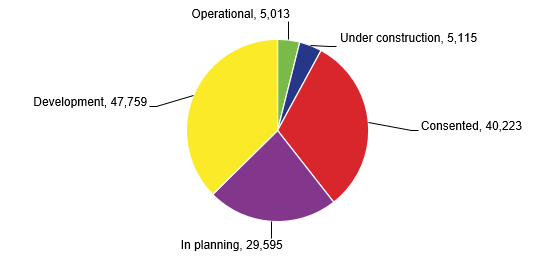

The UK’s total battery storage project pipeline currently contains a total of 127GW of capacity. Figure 1 demonstrates the amount of capacity at each development stage as a proportion of the total pipeline. 8% of the capacity pipeline in the UK is operational or under construction, with 31% approved and yet to begin construction. The remaining 61% of capacity within the pipeline are projects that have either submitted an application and awaiting a decision, or at an early stage of development such as screening or scoping.

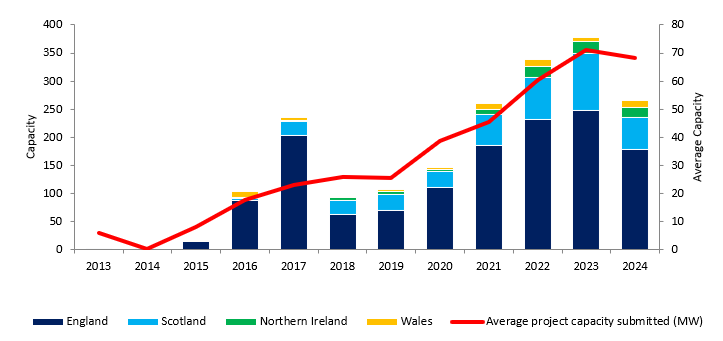

Figure 2 illustrates the trend in commissioning of battery storage projects in the UK. Over the last decade, England has seen the majority of commissioning of battery storage projects (83% since 2013). However, in the past 4 years Scotland, Northern Ireland and Wales have all seen commissioning taking place, accounting for 20% of commissioned capacity in that time. The average capacity of projects being commissioned has been steadily rising since 2015 (when no battery storage capacity was commissioned), to a high in 2023 of just over 33MW.

Figure 2: Capacity commissioned by country (MW) and average capacity per project (MW)

Figure 2: Capacity commissioned by country (MW) and average capacity per project (MW)

In 2023, we witnessed the highest number of planning applications for battery storage projects since records began (Figure 3). Depending on the number of applications submitted in December, 2024 could be set to be the first year since 2018 where the number of applications has not surpassed the previous year; there would need to be more than 100 projects submitted to eclipse the total of 2023. 2024 is also set to see a small decrease in the average capacity of the projects being submitted, currently a 5MW decrease from 71MW in 2023 to 68MW in 2024 year-to-date. I will be reporting on the final 2024 totals alongside much more detailed analysis in the EnergyPulse May 2025 Energy Storage Report. This report will be launched to coincide with Clean Power Grid Conference 2025, 1 May 2025 at the IET, London.

Overall though, the breakdown of the battery storage pipeline in the UK indicates a position of growth, with a large proportion of the pipeline capacity in early development, in planning and consented stages. With just over 5GW of capacity currently under construction, we could reasonably expect battery storage capacity in the UK to reach over 10GW in the next few years.

While capacity commissioned in 2024 is less than that commissioned in 2023, the overall trend is upward, and battery storage continues to see both large- and small-scale applications submitted and approved. England continues to dominate the UK in terms of battery storage although Scotland, Wales and Northern Ireland are showing signs of becoming more involved year-on-year.

How can I access this data?

EnergyPulse stores and provides this data via RenewableUK membership or via subscription. Alongside up-to-date information, EnergyPulse also provides a modelled forecast of how the pipeline will look in years to come, as well as a plethora of data points for global offshore wind and UK onshore wind, battery storage and hydrogen markets. In future editions of this blog, EnergyPulse will also explore grid connection dates, application approval rates, trends in colocation of projects and much more.

If you have any questions, comments or requests about this data or EnergyPulse in general please get in touch with me via email and I would be happy to help.

Related content

About EnergyPulse

RenewableUK’s EnergyPulse is the industry’s go-to market intelligence service for renewable energy news, project data and analysis. Delivering comprehensive and accurate renewable energy data, insights and dashboards for the wind, marine, energy storage and green hydrogen sectors in the UK – and offshore wind globally.

Data correct as of 09/12/2024

Disclaimer

Data is accurate to the best of RenewableUK’s knowledge and is a high-level snapshot of the information available in the renewable energy database. Projections do not represent a RenewableUK position and should be used only as guides to possible outcomes. RenewableUK takes no responsibility for losses incurred by the use of this information.