Daniel Sutherland and Max Bradbury

07/02/2025 | EnergyPulse

UK wind and global offshore wind: 2024 in review

7 February 2025 - EnergyPulse blog

This 2024 review blog covers key statistics and developments in the UK wind sector and the global offshore wind industry through the end of 2024. With the UK positioning wind energy as the backbone of its future energy system, and many other nations adopting similar strategies, the industry continues to experience rapid growth, albeit at a pace that falls short of ambitious targets.

This blog explores UK onshore and offshore wind energy, and provides an overview of statistics and trends in the global offshore wind market.

Related content

UK wind

Onshore

Operational onshore wind in the UK currently totals 15.7GW, increasing by 739MW in 2024 due to the commissioning of some large-scale projects such as, Viking (443MW), Kype Muir Extension (67.2MW) and Broken Cross (43.2MW). These examples are all located in Scotland, but there have been projects completed in the rest of the UK such as Murley, Northern Ireland (21.6MW) and several single turbine projects across Wales. In England most recently, Alaska Wind Farm (8MW) has begun producing power after initially being submitted for planning back in 2009. The capacity under construction perhaps paints a different picture, with just 898MW under construction in the UK. Projects such as Stranoch 2 (102MW) and Crystal Rig IV (48.2MW) entered construction in 2024.

In 2024, 77 onshore wind projects submitted for planning permission including Aultmore, Alwen Forest and the repowering of Bears Down. Slightly down on the 83 submissions of 2023 but substantially more than the 44 submissions in 2022. Large scale projects in England remain scarce, however there are currently 2 projects in early development stages. Cubico’s Scout Moor 2 (21 turbines producing 100MW) and Worldwide Renewable Energy’s Calderdale (65 turbines producing 302MW) have each submitted scoping documentation to local authorities with the latter receiving a scoping direction in December 2023.

According to the EnergyPulse forecasting model [1], the UK is set to achieve 26GW of onshore wind by 2030, 3.1GW below the target set out in the UK Government’s Clean Power 2030 Action Plan (CP30). It will be the goal of the Onshore Wind Industry Task Force to achieve this target by “identifying and then delivering the actions needed to accelerate onshore wind deployment to 2030 and beyond”. The forecast for 2035 exceeds the CP30 Action Plan’s target of 37GW, predicting a total of 39.5GW.

Map of UK onshore wind projects viewed on the EnergyPulse UK Wind, Storage and Hydrogen dashboard

UK offshore wind

The UK's current operational offshore wind capacity stands at 14.7 GW. Notably, 2024 marked the first year since 2016 without any new offshore wind projects fully commissioned. However, significant construction activity continued offshore, with six projects totalling 6.3GW undergoing major offshore installation activities. Among these, three projects (2.5GW) are expected to reach full commissioning in 2025, while two more (2.5GW) will begin major offshore construction during the year.

Map of UK operational and planned offshore wind projects, viewed on our EnergyPulse dashboards

-

Learn more about trends in UK onshore and offshore wind

How can I access this data?

EnergyPulse stores and provides this data via RenewableUK membership or via subscription.

The number of offshore wind planning applications in the UK saw remarkable growth in 2024, with the capacity of projects in the UK’s planning systems nearly tripling. Fourteen planning applications, representing 15.4GW, were submitted, bringing the total capacity in the planning system to 22.85GW by year-end. Four projects (1.3GW) received planning consent in 2024.

EnergyPulse forecasts that UK offshore wind capacity will reach 41.5GW by the end of 2030, including partially commissioned projects, with fully commissioned capacity predicted at 36.8GW. This includes 1.2GW of floating wind capacity, although much of this hinges on a few key projects currently scheduled for 2030 completion.

Global offshore wind

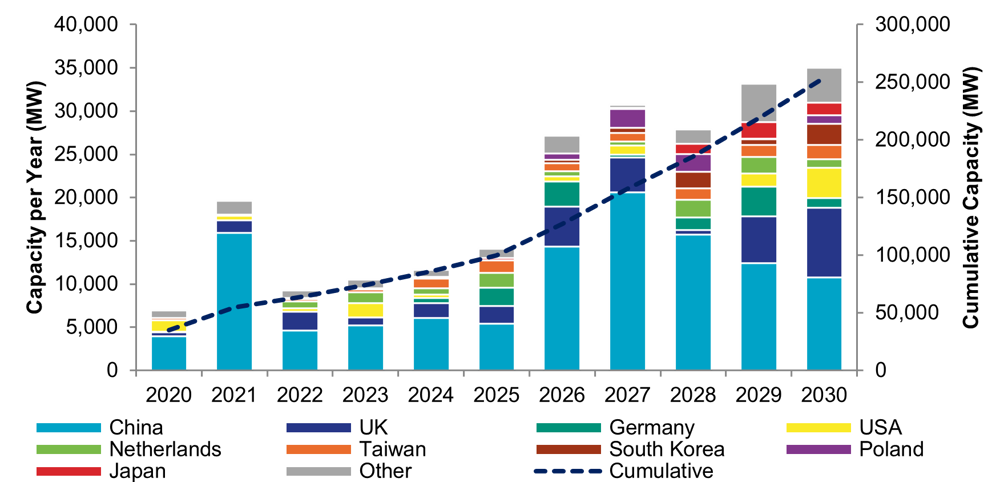

By the end of 2024, the global capacity of fully commissioned offshore wind projects stood at 80.9GW, with a further 6.6GW partially operational. For the first time, China accounts for more than half of the world’s fully commissioned capacity, surpassing 41GW, although this market share is expected to decrease as new markets expand.

Global offshore wind capacity forecast by country

EnergyPulse forecasts that global offshore wind capacity will reach 254GW by the end of 2030, including partially operational projects. 120GW of this is expected to be in China. Achieving this global forecast requires an impressive threefold increase from the capacity at the end of 2024, although this projection suggests that many countries will fall significantly short of their centrally announced offshore wind targets. The majority of offshore wind capacity through 2030 will come from already established markets. By the end of 2024, 19 countries had installed offshore wind turbines, with only three additional countries expected to join this group by 2030.

China’s influence is also growing internationally, with Chinese companies securing development rights in South Korea and Indonesia in 2024. Three Chinese foundation fabricators were awarded contracts for European projects, Cable fabricators, Hengtong and Orient Cable, were awarded cable supply contracts in South Korea and the UK respectively, whilst Mingyang was selected as the preferred supplier for turbines on projects in Germany and Italy and multiple Chinese turbine suppliers mentioned in winning bids for European sites.

Early-stage interest in offshore wind continues to increase, despite market challenges. In 2024, a total of 88.5GW of site exclusivity leases were awarded across 12 countries, spanning both established and emerging markets. The top three markets for exclusivity awards were Australia (28.3GW), China (20.7GW), and the United States (14.2GW).

Advancing through the development pipeline, 53.9GW of capacity received full Environmental Impact Assessment (EIA) approval across 10 countries. Leading the approvals were China (20.2GW), the United States (9.9GW), and South Korea (7.3GW). The final consented project of the year, Wando Jangbogo in South Korea, achieved full EIA approval on 31 December.

Of the 18.9 GW of firm offshore turbine awards in 2024, Vestas leads with 5.9GW awarded, followed by Goldwind (3.6GW) and Siemens Gamesa (2.7GW).

-

Discover more trends in global offshore wind

How can I access this data?

EnergyPulse stores and provides this data via RenewableUK membership or via subscription.

Methodology

[1] This blog consists of analysis and forecasts of project milestones, capacity, turbine numbers, and ownership for UK onshore wind farms greater than 100kW in size. All data is sourced from publicly available information.

Where real dates and values are known, they are represented in the data. Unknown dates and values are modelled using assumptions and trends derived from the installed base of UK onshore wind projects. Our model uses historical data trends including the time taken for a project to receive a planning decision, length of appeal, time from consent to construction and time taken to construct and commission. The data is refined by project size and geography where appropriate. Every effort has been made to present the most up-to-date information obtainable prior to publication. Projects in planning or early-stage development are assumed to receive consent. Valid consented projects are modelled as always being built.

Our forecasting model does not make any assumptions on the timing of commissioning where there are conditions attached to a consent that relate to aviation constraints or Eskdalemuir exclusion arrangements. Where an estimated grid connection date is known then this is used to refine the timings of the model.

Projects that have received a planning consent, but according to our research have not been progressed to construction by the date stipulated in conditions of a consent, are not include in projections of future capacity or the totals of consented projects used throughout the blog unless otherwise stated.

About EnergyPulse

RenewableUK’s EnergyPulse is the industry’s go-to market intelligence service for renewable energy news, project data and analysis. Delivering comprehensive and accurate renewable energy data, insights and dashboards for the wind, marine, energy storage and green hydrogen sectors in the UK – and offshore wind globally.

Data correct as of 5 February 2025.

Disclaimer

Data is accurate to the best of RenewableUK’s knowledge and is a high-level snapshot of the information available in the renewable energy database. Projections do not represent a RenewableUK position and should be used only as guides to possible outcomes. RenewableUK takes no responsibility for losses incurred by the use of this information.