01/05/2024 | Energy storage

UK energy storage pipeline report 2024

RenewableUK EnergyPulse report - May 2024

Foreword by Yonna Vittonova, Senior Policy Analyst

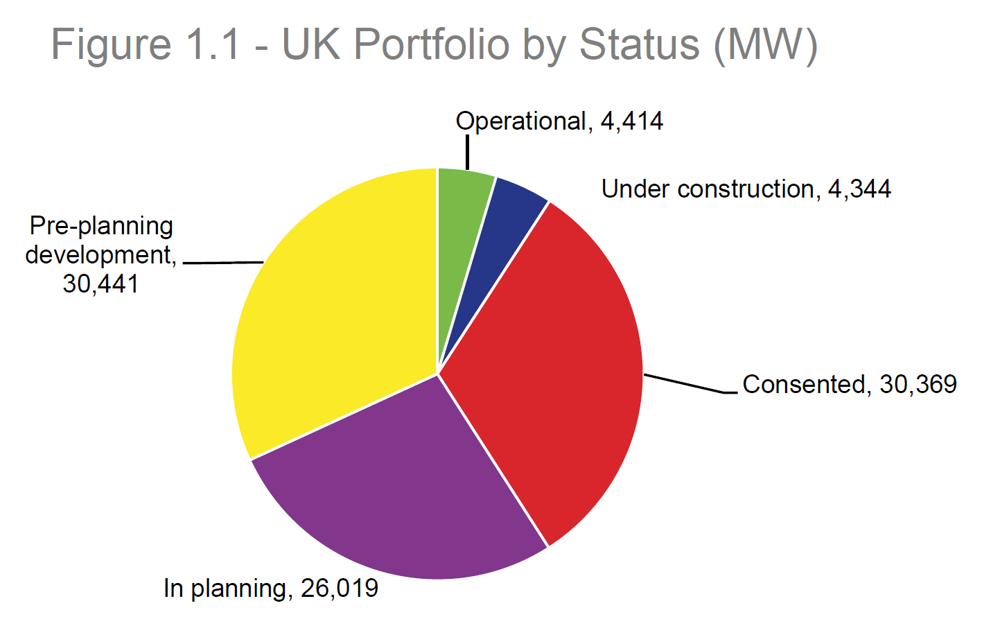

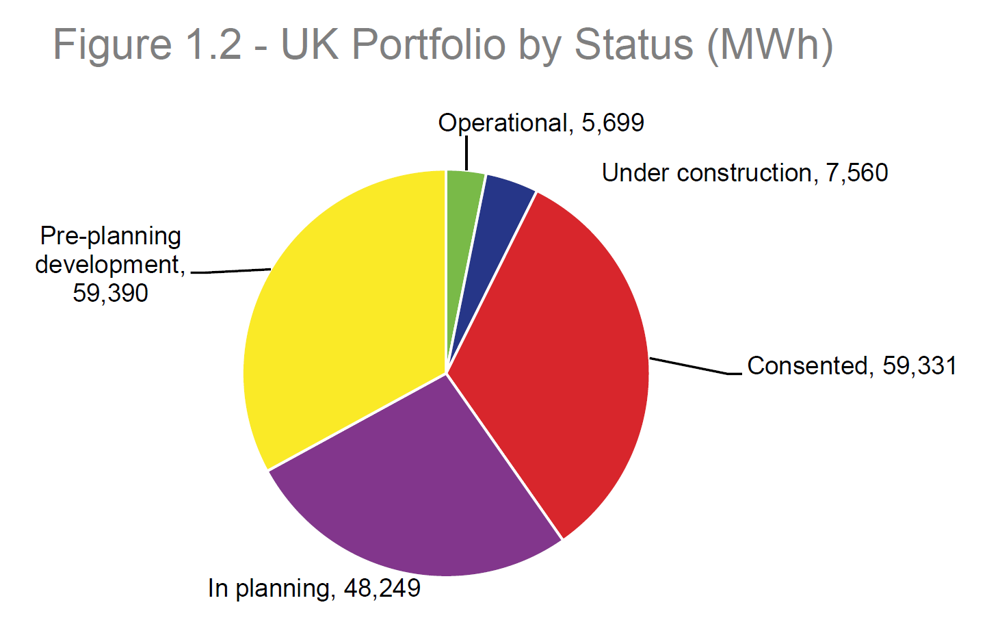

The pipeline of battery storage projects has continued to grow steadily again, from 84.4GW in December 2023 to 95.5GW in May 2024. This edition of the EnergyPulse report on Energy Storage shows there is 8.7GW of batteries in operation and under construction and more than 30GW projects have now been consented. While there has been significant uptake in projects, we are long way from delivering up to 55GW of short-term flexibility by 2035 as outlined in the DESNZ Review of Electricity Market Arrangements.

Battery storage continues to play an important role as fast acting flexibility providing a range of grid services. Despite the staggering growth, the business case for projects is becoming even more difficult as balancing markets saturate. NGESO roll out of the Balancing Reserve, the additional measures to address batteryskip rates in the Balancing Mechanism and the work to introduce new parameters to optimise dispatch and planning will be critical to address the growing risk of oversaturated balancing markets.

While this growth is positive for the battery sector, it is also driving up the connection queue: there is now over 700GW of capacity waiting for a connection, much of this storage, and connection dates are being offered in to the late 2030s. Reform of the connection process is urgently needed to identify and prioritise those projects with the best prospects of coming online.

There has been a shift in the pipeline for current and future long duration electricity storage (LDES), from over 7.2GW in December 2023 to 10.5GW in May 2024. In January, the Government published its long-awaited consultation on the cap and floor revenue stabilisation mechanism for LDES. Timely technology neutral design and allocation of cap and floor would serve to unlock opportunities across a wide range of LDES technologies. Industry is also eagerly awaiting the Government decision on reforms to allow new, long lead time LDES projects to compete in T-4 auctions and manage battery degradation within the Capacity Market.